The State Tax Service excluded the sole proprietor from the single tax payers register: The Supreme Court put the decision on hold

In tax dispute practice, the issue of securing a claim often becomes a key tool for protecting business during lengthy court proceedings. It essentially determines the taxpayer's ability to maintain operational stability during the appeal of decisions made by controlling authorities.

For a long time, courts of first instance cautiously approached the adoption of such measures in tax cases, fearing interference with the discretionary powers of the State Tax Service (STS). Case No. 520/25465/25, reviewed by the Supreme Court on May 21, 2026, in a panel of judges of the Cassation Administrative Court, set priorities. The protection of the plaintiff's substantive legal interests takes precedence over the formalistic approach of the controlling authority.

The essence of the dispute

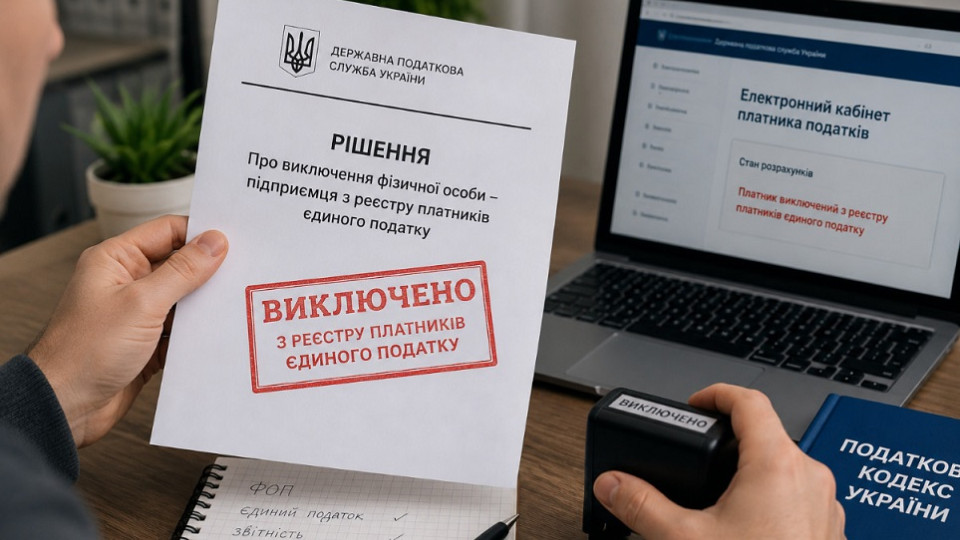

The Main Department of the STS in Kharkiv Region made a decision to annul the registration and exclude the sole proprietor from the Register of single tax payers.

The entrepreneur appealed to the Kharkiv District Administrative Court demanding the cancellation of this decision and reinstatement in the Register as a single tax payer of the second group. Along with the lawsuit, an application was filed to secure the claim by suspending the STS decision until the final court ruling comes into force.

The sole proprietor justified the claim by excessive burden. The automatic transition to the general taxation system entails the obligation to pay 18% personal income tax and 20% VAT retroactively from the beginning of the year. For failure to submit VAT declarations for previous months, significant fines will be imposed on the plaintiff.

Moreover, partners confident in cooperation with a single tax payer will likely terminate contracts due to the unpredictable change in tax status. Even if the court is won after a year, the financial and reputational losses will be so significant that restoring business activity will be almost impossible.

The court of first instance refused to secure the claim, considering the sole proprietor's evidence insufficient. However, the Second Administrative Court of Appeal overturned this ruling. The appellate court concluded that failure to adopt securing measures would significantly complicate or make impossible the effective protection of the plaintiff's rights. The court noted that suspending the STS decision is aimed solely at preserving the existing situation until the case is examined on the merits. The tax authority, disagreeing with this, filed a cassation appeal to the Supreme Court.

Supreme Court decision

The Supreme Court, having examined the arguments of the STS cassation appeal, left the appellate court's decision unchanged.

According to Article 150 of the Code of Administrative Procedure of Ukraine, securing a claim is allowed in cases where failure to take such measures may significantly complicate or make impossible the execution of a future court decision or the effective protection of the plaintiff's rights.

Another basis for securing is the presence of signs of obvious illegality of the decision of a public authority. The Supreme Court has repeatedly emphasized that these criteria are evaluative, so the court in each case must balance the interests of the parties.

According to Article 151 of the Code of Administrative Procedure of Ukraine, securing measures must be proportionate to the claims made and cannot exceed what is necessary for the effective protection of the right.

In the case under consideration, the suspension of the decision to annul registration as a single tax payer was applied as a temporary measure. It does not resolve the dispute on the merits but aims to prevent possible irreversible negative consequences for the taxpayer until the final decision is made.

The court also referred to the Council of Europe Recommendation No. R (89) 8 on provisional judicial protection, according to which securing measures may be applied in cases where the execution of an administrative act may cause significant harm, the compensation of which would be difficult or impossible.

Specifics of tax legal relations

The court separately drew attention to the provisions of paragraphs 299.10 and 299.11 of Article 299 of the Tax Code of Ukraine, which regulate the procedure for annulling the registration of a single tax payer.

Since the change of the taxation system affects not only the taxpayer but also their counterparties, in particular due to the need to adjust the VAT tax credit, failure to take securing measures could cause chain negative consequences in tax legal relations.

The tax authority in the cassation appeal argued that the sole proprietor's application lacked sufficient justification. However, the Supreme Court emphasized that the validity of the claim itself is not examined at this stage — this is the subject of the case on the merits.

The main task at the stage of securing the claim is to ensure the reality of the threat of difficulty in executing the future court decision.

The Supreme Court ruling in case No. 520/25465/25 is of great importance for protecting business from the consequences of decisions by controlling authorities. The court confirmed that the institution of securing a claim is not a formal procedural procedure but a real mechanism guaranteeing effective judicial protection.

Forced change of the taxation system can create significant financial risks for the taxpayer, in particular due to the need to switch to the general taxation system, the emergence of additional tax liabilities, and possible penalties for previous periods. Such consequences may indicate the presence of a risk of significant harm, which is grounds for applying securing measures.

The Supreme Court also confirmed legal approaches previously formulated in cases No. 280/8758/24 and No. 420/25688/24, indicating the formation of a stable judicial practice regarding the protection of taxpayers in similar disputes.

Subscribe to our Telegram channel t.me/sudua and to Google News SUD.UA, as well as to our VIBER and WhatsApp, page on Facebook and on Instagram to stay updated on the most important events.